Synthetix v3 Investment Thesis

Introduction

The way I see it, Synthetix is a liquidity hub that allows other protocols like Kwenta and Polynomial to plug in and use their liquidity for creating markets for trading of financial products like spot, perpetuals, options etc. Synthetix aims to solve the cold start problem for DeFi protocols which refers to the challenge of bootstrapping initial liquidity and attracting users to the platform. Liquidity is a crucial factor for the success of any DeFi protocol, as it ensures that there are enough buy and sell orders available for users to execute trades at fair prices and without significant slippage.

Investment Thesis:

Synthetix V3 will expand beyond SNX staking and allow for multi-collateral staking which will increase sUSD liquidity

Differentiated debt pools will result in better risk management as stakers will no longer be exposed to a singular SNX debt pool

Integration of CCIP will expand Synthetix to additional EVM-compatible chains like Arbitrum which will further increase the addressable market

Frontends like Kwenta and Infinex can focus on acquiring users without having to worry about liquidity

Perps V3

Investment Risks:

This system is still inherently capital inefficient

Current trading volumes are motivated by trading incentives

Frontends are unprofitable

Death spiral?

Thesis

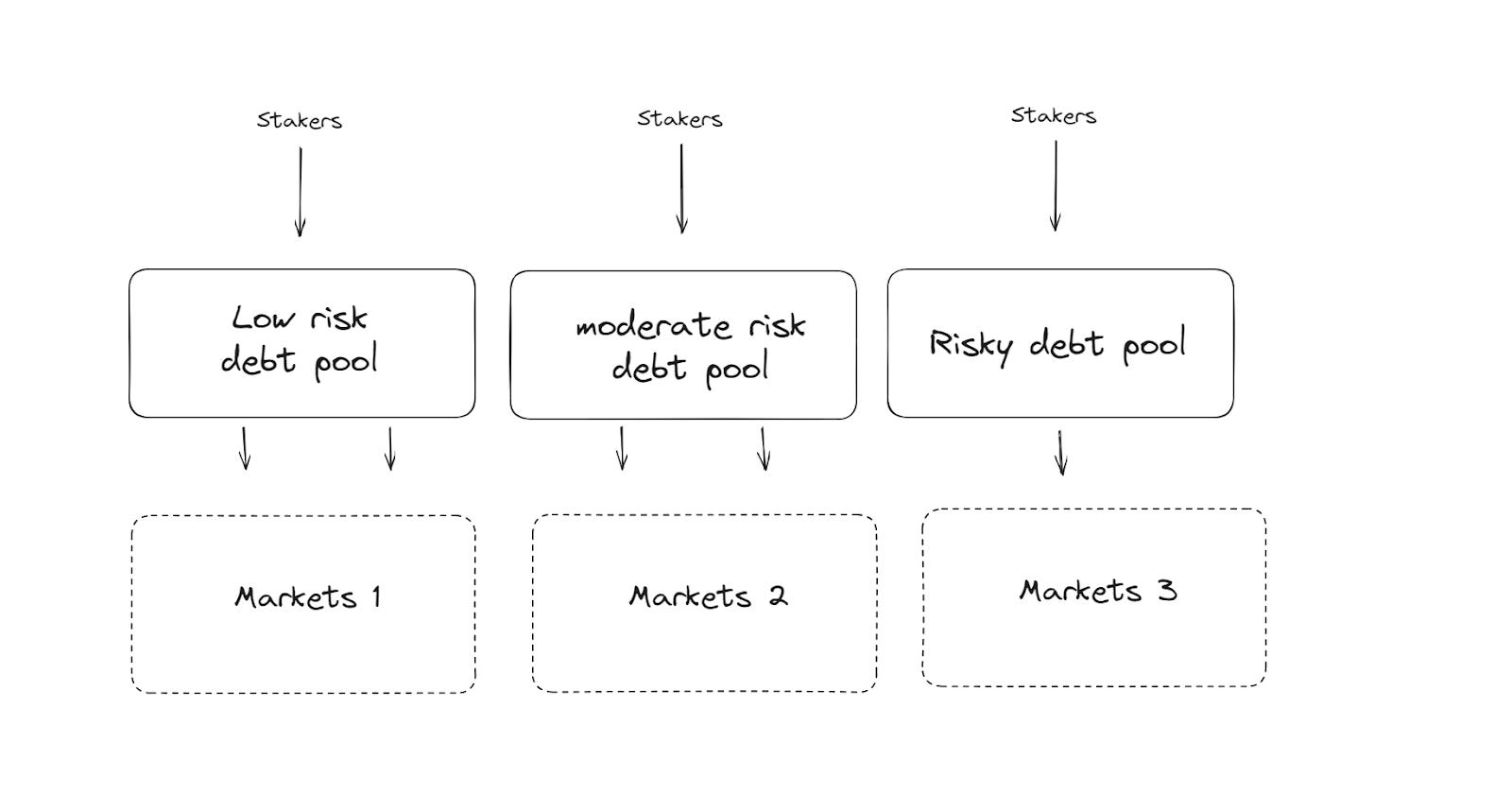

Multi-collateral Staking and Differentiated debt pools

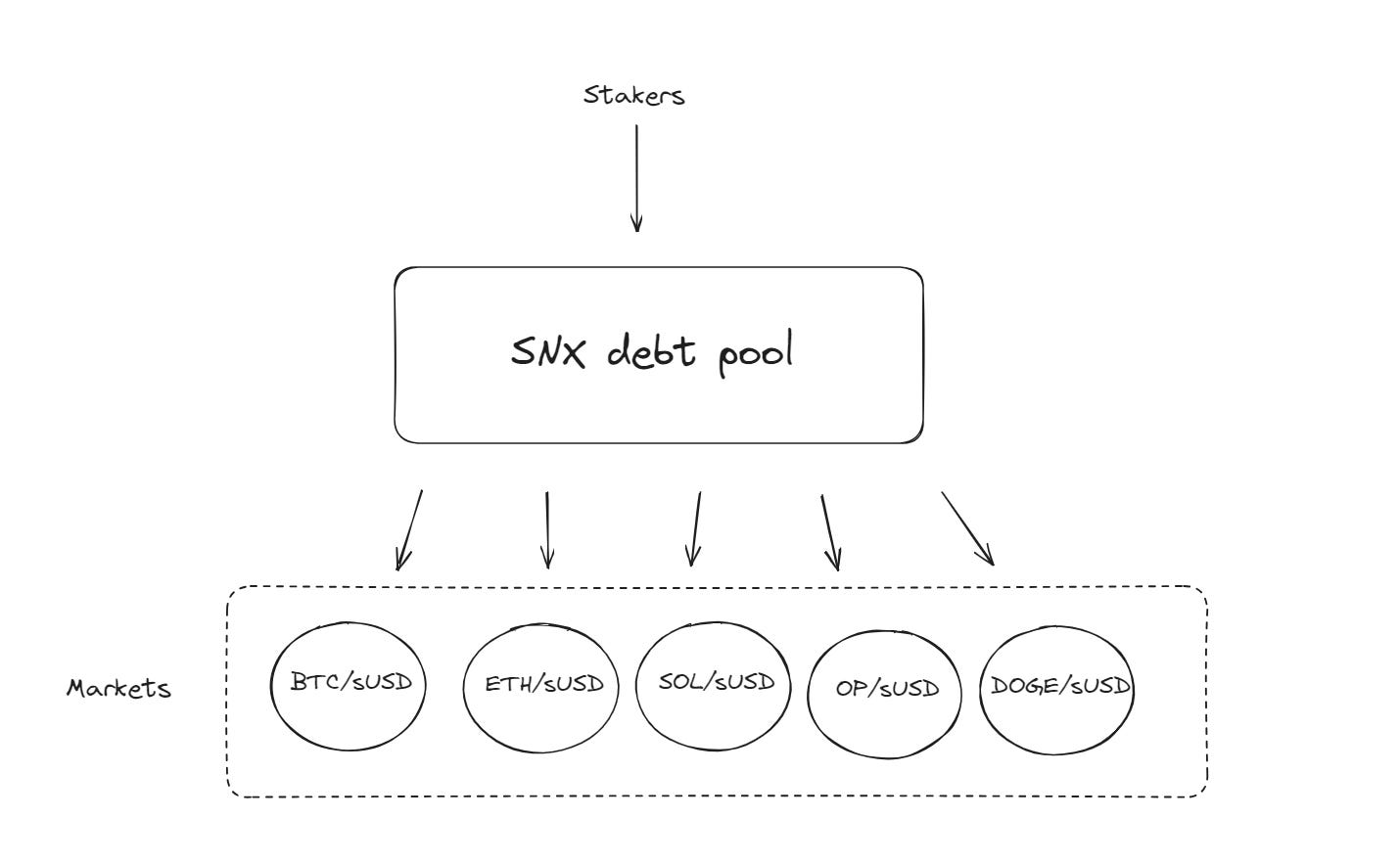

In essence, differentiated debt pools have two main benefits - risk segregation and customized risk exposure. In Synthetix V2, there was a sole SNX debt pool which supported multiple markets. For instance, SNX stakers and the debt pool has exposure to Kwenta’s various trading pairs as seen below. To recap how Synthetix works in simple terms - if the pool takes on counterparty risk, traders losses = profit for SNX stakers, traders profits = losses for SNX stakers. Hence, the exposure to so many different markets with varying volatility is actually a substantial risk for the debt pool. The system relies on efficient arbitrage, volatility needs to remain smooth enough that arbitrage happens efficiently as traders enter, exit or get liquidated. In an event of black swan level of volatility, the SNX pool might be exposed to a significant amount of counterparty risk.

With the launch of V3, stakers will be able to isolate their exposure to assets that they choose. For example, a staker who only wants exposure to ETH can set up an ETH liquidity provisioning position and capture the fees from that, as opposed to the undifferentiated pool of every single asset previously.

Furthermore, an inherent challenge with SNX serving as the sole accepted staking collateral lies in its capacity to limit scalability. This constraint arises from the fact that the economic bandwidth of the protocol is ultimately determined by the market cap of SNX. If other collaterals like ETH are accepted, Synthetix will be able to scale their operations.

Cross chain integration

The integration of Chainlink Cross-Chain Interoperability Protocol (CCIP) into Synthetix V3 will allow sUSD to be minted on any EVM compatible chain. What this means is that there will be Synthetix liquidity not just on Ethereum and Optimism but on other EVM chains as well. Expanding further on this, debt created on chain A can be paid off by the stablecoins on chain B. This also unlocks a wider degree of interoperability with pools on Chain A being able to back a market on Chain B. Synthetix is also exploring the usage of Chainlink CCIP for additional use cases, including cross-chain synthetic perpetual futures, cross-chain staking pools, and more. These plans to expand beyond Ethereum and Optimism effectively increases the total addressable market size for Synthetix.

Permissionless Markets

Synthetix founder Kain has often referenced the centralized exchange playbook over the years. It’s essentially the idea that the way you win a market cycle is by having the assets that people want to trade as quickly as possible. In 2017, exchanges like Coinbase, Kraken and Bitfinex were so entrenched that nobody thought any new exchanges could touch their moat. During the ICO phase, Binance adopted the strategy of listing every ICO token as quickly as possible and made it the to-go exchange for all tokens. Naturally, users started to move their trading activities over to Binance. This is a powerful network effect strategy that Synthetix aims to emulate. Kain brought up the example of the listing of meme coin PEPE that sparked off a lot of trading volume for exchanges. Synthetix wanted to list it as quickly as possible but ended up still being about three weeks later than Binance.

It’s evident that Synthetix is hoping to emulate this successful playbook. However, earlier impediments that prevented them from doing so are oracles and other technical overhead. Why are oracles still the main hurdle? To put it simply, there’s no way Synthetix can offer markets for PEPE if Chainlink or Pyth does not have PEPE price feeds available. Secondly, new markets were required to pass through governance before they got listed in order to protect SNX stakers. For example, See the governance proposal SIP-2014 for PEPE, SUI & BLUR here. After scouring through governance proposals and forum discussions to understand the community’s considerations for new market listings, it really boils down to few main factors in order to prevent another Eisenberg-esue exploit - (a) high trading volume and liquidity, (b) perp listing on tier 1 centralized exchanges and (c) even better if there’s a perp listing on centralized exchanges. With differentiated debt pools, the hope is that longer tail “riskier” markets can be allocated to “riskier” pools that stakers will be aware of before getting themselves involved.

Front end optimization

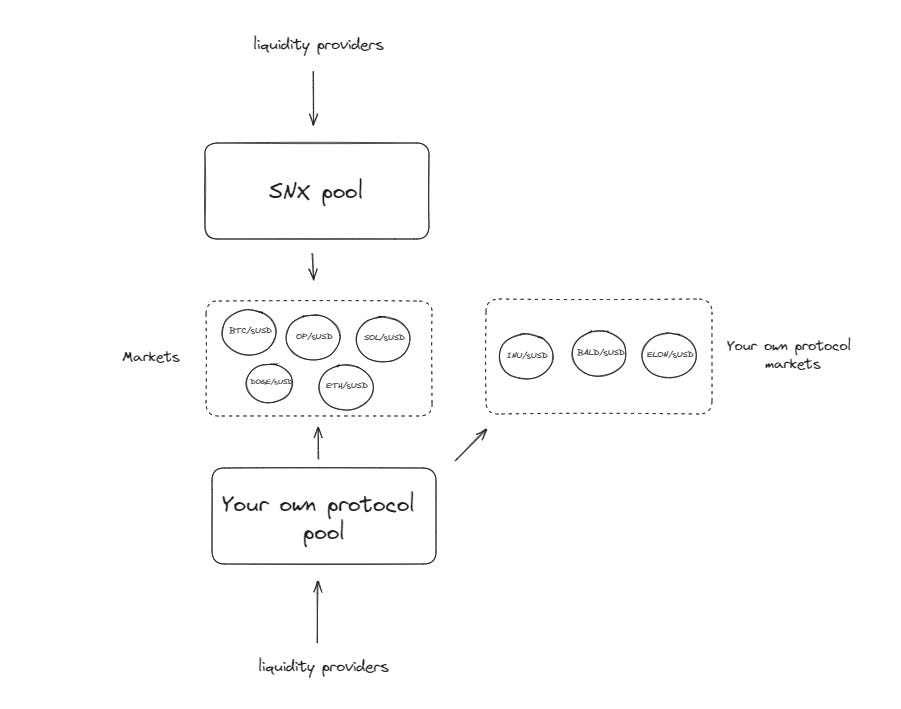

Synthetix plays a crucial role as a liquidity layer enabling front-end applications like Infinex and Kwenta to seamlessly plug in and focus on user acquisition without the burden of managing liquidity. By leveraging Synthetix, these front-end platforms can offer their users access to a diverse range of synthetic assets without having to worry about setting up their own liquidity pools. Additionally, the ability to spin up your own pools and accept other collaterals outside of SNX opens up more possibilities for protocols to control their own liquidity in the future.

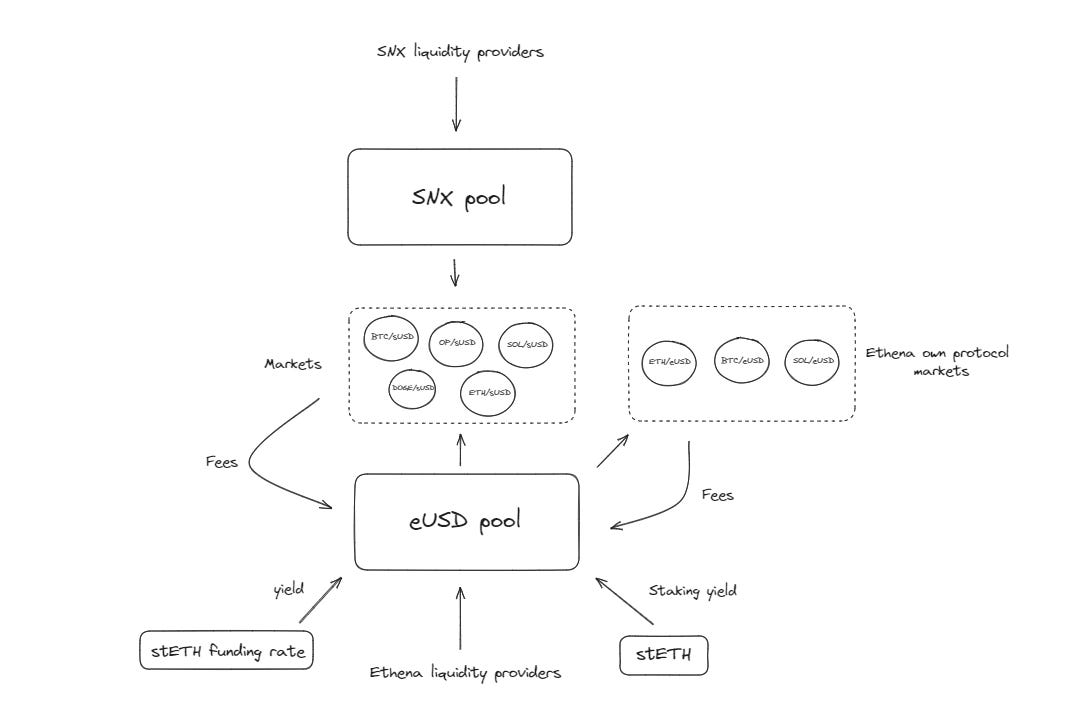

Let’s take a deeper look at one of the upcoming protocol integrations with Synthetix v3 to understand further. Ethena is crypto-native stablecoin which ensures stability through delta-neutral hedging process across both CEXes and DEXes. One of the crucial reasons why Ethena has chosen to build on top of Synthetix v3 is the ability to use stETH as a collateral for their on-chain perpetual hedging operations. As seen in SIP-2031, this will allow Ethena to open short ETH positions directly with stETH which is currently not possible on CEXes at the moment. Other key reasons include the presence of existing deep liquidity and perp trading volume within the Synthetix ecosystem, orderbook depth/ execution references CEXes depth as oracle, and funding mechanics are well thought through and favourable to allow for stability.

The integration of Ethena is also beneficial to Synthetix. The introduction of permissionless pools will potentially allow for new collateral forms like ETH, stETH and even Ethena’s USDe. Ethena is not only a good source of trading volume for Synthetix Perps but if governance decides to include USDe as an acceptable collateral, it opens up more possibilities for users and also more revenue sources for SNX holders. The end result could look something like the diagram below

Another great example would be Rage Trade’s upcoming v2. While Synthetix solves the problem of cold start liquidity for perpetual frontends, user experience is the other side of the equation that Rage Trade aspires to solve. One of Rage Trade’s key focus areas will be a prime broker perps aggregator model. Rage Trade aims to abstract away the idea of multiple perps on multiple separate chains to create a unified experience to trade on all perps across any EVM chain. Additionally, users are able to access features such as cross position margining and being able to open positions with multiple collaterals. The end result? Users are able to enjoy best price and funding execution as well as access to token airdrops across multiple perp platforms.

Perps V3

There were three main changes in perps v2 that helped increase trading volume for Synthetix - (1) lower fees by transitioning to off-chain oracles, (2) price impact function and (3) dynamic funding rates. I will only be discussing dynamic funding rates here in detail because it’s the biggest game changer in my opinion.

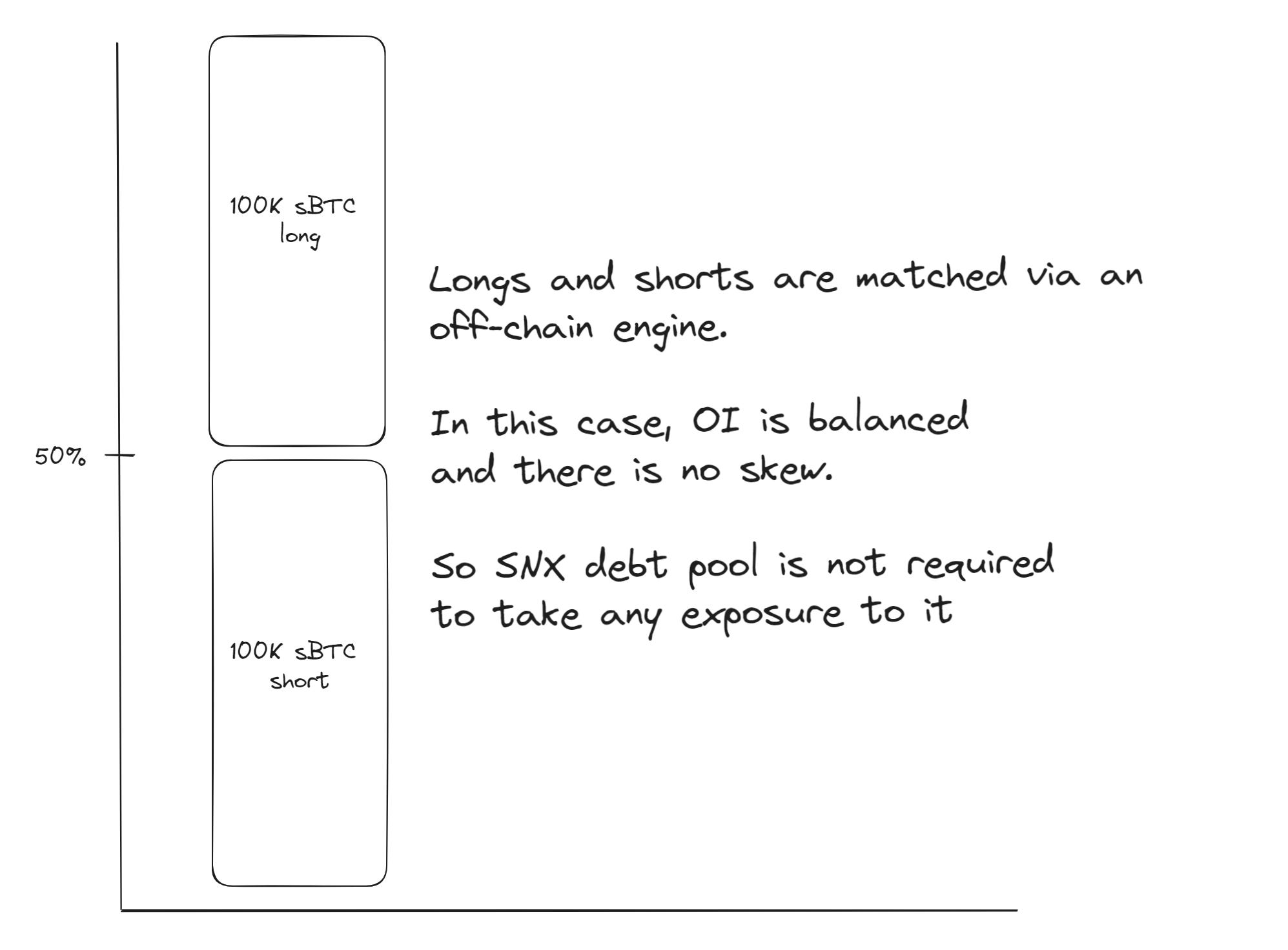

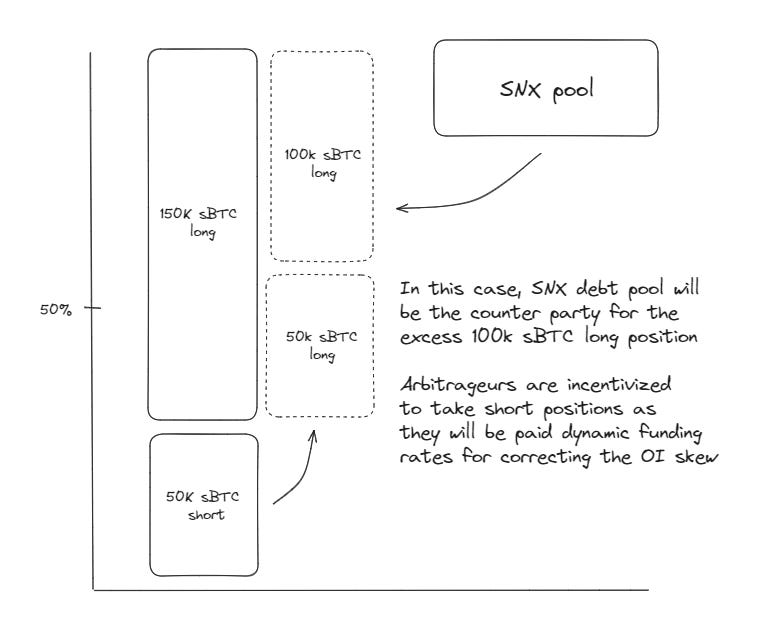

While funding rates were meant to ensure that there is a balance between long and short positions, actual implementation showed that this mechanism alone was not sufficient. Other oracle based perps like GMX also had the problem of imbalance skew which resulted in exposure of their liquidity providers. Perps v2’s dynamic funding rate aimed to solve this problem. The dynamic funding rate considers both velocity and market skew. This implies that in the presence of a prolonged positive skew, funding rates will progressively rise. Conversely, if short positions are prevalent and the short skew remains, funding rates will decline. By integrating velocity into the funding rate computation, this system incentivizes traders to assume positions that counteract the prevailing market skew. Over the past few months, the open interest has consistently stayed within a narrow range of approximately 50%

How does this result in better risk management for SNX stakers? The following diagrams show why a balanced open interest is ideal and how perps v2 can help to correct the imbalance skew.

Risks

This system is still inherently capital inefficient

Synthetix has been criticized for being capital inefficient primarily due to its reliance on over-collateralization as a mechanism to secure the synthetic assets created on the platform. The Synthetix protocol requires users to lock up a significant amount of the native SNX token as collateral to mint synths. This collateralization ratio is typically around 500%, meaning that to create $100 worth of synthetic assets, a user would need to lock up around $500 worth of SNX. The capital inefficiency arises from this high collateralization ratio. It means that a substantial amount of capital is locked up as collateral, which could otherwise be used for other purposes or invested elsewhere. From another point of view, it can also be argued that this over-collateralization mechanism only affects liquidity providers and SNX stakers. The majority of users of Synthetix front ends only has to purchase sUSD from the open markets instead of minting it.

Current trading volumes are motivated by trading incentives

The current trading volumes on Synthetix are to some extent propped up by token incentives provided by platforms like Optimism and Kwenta. These incentives are designed to encourage users to participate in trading activities on the Synthetix protocol, leading to increased trading volumes. While these incentives have undoubtedly contributed to the growth of trading volumes, it is essential to recognize that they might not entirely reflect true trader demand or the organic usage of the platform. Some participants might be primarily motivated by the token rewards rather than having genuine interest in trading synthetic assets, potentially skewing the overall trading activity on the platform.

Token incentives can be an effective user acquisition strategy, as they attract new users to the platform and incentivize existing users to remain engaged. These incentives create a powerful marketing tool, driving interest and participation in the protocol, which is crucial for the growth of any ecosystem. However, there is a potential downside to relying heavily on token incentives. By offering attractive rewards, the protocol might attract users who are solely interested in earning tokens rather than evaluating the platform's utility or long-term value proposition. This influx of users driven by incentives might mask the true product-market fit, making it challenging to gauge whether the protocol is genuinely addressing user needs and demands. To discover true product-market fit, it is essential for the protocol to attract users who find value in the platform beyond the token rewards, and that requires a more organic and sustainable approach to user acquisition.

Front ends are unprofitable

Current front ends like Kwenta and Polynomial are paid between 5-10% of total volume in native SNX tokens by the Synthetix Treasury via Partners Volume Rewards scheme.

However, frontends within the Synthetix ecosystem are still reportedly operating at a loss, since all trading fees are accrued back to SNX stakers. It’s evident that there needs to be more incentives in order to attract high quality front ends to build on top of Synthetix in the future. As part of perps v3, a new fee structure allows front ends to either implement their own fees or receive a percentage of fees similar to how GMX does it. For instance, Polynomial has an additional fee on top for stop/limit orders. This potential fee-sharing concept is viewed as a step towards financial sustainability and maintaining a focus on SNX integration. Whether this new proposed fee structure will lead to an overall higher amount of revenue accrued back to SNX holders remains to be seen.

Death Spiral?

Synthetix's stability and success as a protocol are heavily dependent on the holders' confidence and belief in the value of the SNX token. As the native token of the Synthetix platform, SNX serves multiple essential functions within the ecosystem. It is used as collateral to mint synthetic assets (synths) and participate in staking to earn rewards. Additionally, SNX holders play a crucial role in governing the protocol through decentralized decision-making.

However, the value of the SNX token is not immune to potential risks. Just like any other tokens, it is subject to market fluctuations and sentiment-driven movements. One significant vulnerability arises from potential exploits or security breaches, similar to what happened to other DeFi projects like Curve Finance or other protocols in the past.

In the event of a similar exploit or security breach that negatively impacts the SNX token's value, it could lead to a loss of confidence among SNX holders. This loss of confidence may prompt some holders to sell their tokens in fear of further losses, causing the token's price to plummet. Such a scenario could result in a negative feedback loop, triggering more selling pressure and potentially destabilizing the entire Synthetix ecosystem.

The instability caused by a significant SNX token value decline could have broader implications for the protocol. For instance, if the value of the collateral (SNX) backing the minted synths falls below the required level, it might lead to under-collateralization, potentially triggering liquidations. This could create cascading effects, impacting users who have minted synths, staked SNX, or provided liquidity to the platform.

What happens when SNX stakers are liquidated? The SNX collateral and corresponding debt is redistributed back to the other SNX stakers. Therefore it can be argued that if some stakers would rather be liquidated than pay off their debt, as long as there is value in the Synthetix ecosystem (i.e. users of Kwenta and other front ends), the remaining stakers are incentivized to claim their debt in order to gain access to their SNX staking rewards.

I do think that the Armageddon death spiral scenario is still a very slim possibility if the value of SNX somehow drops 80-90% within a short period of time that inflicts bad debt for the majority of the stakers.

Conclusion

Ultimately, Synthetix v3 is an overall exciting progress for the protocol. While its implementation will take a while, I truly believe that it will continue to build Synthetix’s moat and add to its overall resilience. One more thing to add - I have been thoroughly impressed by the Synthetix community and how involved they are in discussing and debating the progress of the ecosystem. The concept of governance and community-owned protocols is truly what differentiates DeFi from TradFi and while Synthetix is a work in progress, I believe they are at the forefront of this shift.