Jito Thesis

While the “Jito = Lido + Flashbots” narrative is widely spoken about, I do feel that it is still wildly underappreciated and misunderstood. What does this business model entail exactly? How does the “Lido and Flashbots” component of Jito complement each other? How does value accrue back to $JTO holders? What is their growth potential? This essay aims to unpack Jito in a succinct manner and subsequently highlighting some of my own investment thesis

Understanding Jito

Underpinning Jito’s entire operations is the Jito-Solana validator client which essentially allows MEV extraction for validators. Jito-Solana validators are able to process bundles which are essentially a list of transactions that executes sequentially and atomically. Highly recommend reading this to fully appreciate how Solana MEV works and how the Jito-Solana validator client is a more efficient way to tackle MEV. Using the Jito-Solana validator client, Jito’s current business model is focused on two primary areas: a liquid staking protocol and a MEV marketplace.

Liquid staking protocol

The liquid staking protocol is what most people know Jito for - their JitoSOL liquid staking token. It is essentially a staking pool that connects stakers and validators. Stakers want to maximize their staking yield and also have access to liquidity at the same time. Validators want to be delegated more SOL stake so they can maximize their reward commissions. Jito takes a 4% cut out of staking rewards and MEV revenue after validator commissions. Note that Solana operates on delegated proof-of-stake so that means unlike Lido who has to convince validators to join their stake pool, Jito can simply automatically delegate to a select group of validators. See the diagram below for the flow of funds.

Attracting stakers to a platform like Jito involves several strategic approaches. Firstly, offering a competitive yield is crucial. While MEV rewards are not exclusive to Jito as other stake pools like Marinade and Blaze are also leveraging Jito clients, Jito only delegates to validators running the Jito clients which means maximizing MEV yield for JitoSOL stakers. Next, expanding the utility of JitoSOL in the Solana DeFi ecosystem, particularly in lending and borrowing protocols like MarginFi, could be a significant draw. Exploring its application in other types of protocols could further enhance its attractiveness. Lastly, the safety of staked assets is a paramount concern. Smart contract risks are a critical consideration, but most staking pools utilizing the SPL Stake Pool Program benefit from thorough audits, ensuring minimal risk. Additionally, issues like the recent mSOL “depeg”, primarily a liquidity problem, are expected to decrease as the supply of LSTs grows along with other efforts such as integration with Sanctum Infinity.

In the future, the staking pool will be improved with the implementation of StakeNet. Most stake pools today including Jito require a centralized way of managing delegation. For instance, validators are selected by Jito Labs based on criteria such as history performance, total stake, decentralization score, commission rate etc. This means if Jito stops actively managing the pool, the staking pool will likely not be able to sustain itself. This is evidenced by how Lido decided to discontinue support of their staking pool and also stSOL. To address this, Jito introduced StakeNet, a decentralized, transparent protocol designed to operate intelligent stake pools, ensuring long-term autonomy and efficiency in Solana DeFi. StakeNet's key features include a Validator History Program for detailed validator records and a Steward Program for optimized stake delegation. In short, a network of keepers will ensure that the staking pool is delegated appropriately. StakeNet can also be utilized by other Solana stakepools to manage their delegation in the future.

MEV Marketplace

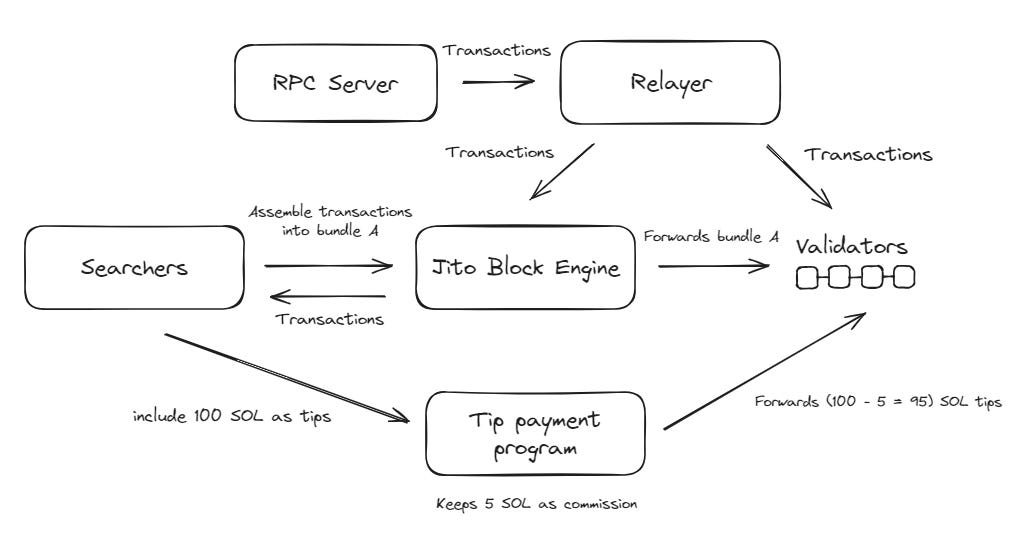

In addition to the liquid staking protocol, Jito Labs has developed an MEV marketplace. This marketplace facilitates the interaction between validators and searchers. Validators running the Jito-Solana client can connect to Jito's Block Engine, enabling them to earn more from traders' bundles. This setup allows validators to optimize their performance on the Solana blockchain and share MEV with stakers to attract more stake. On the other hand, searchers can leverage Jito's Block Engine, Bundles, ShredStream, and APIs to enhance their trading strategies and maximize profits. The aim here is to optimize the MEV market while providing robust defenses against spam transactions that often cause network congestion and disruptions. The revenue model here is fairly straightforward as the Jito Block Engine takes a 5% cut of the tips that searchers send to validators. Do remember that the Jito-Solana client is also adopted by validators participating in other stake pools so this represents a significant potential source of revenue.

This MEV marketplace faced a chicken-or-egg cold start problem which the Jito team managed to crack. Searchers will not participate if there are few validators using the Jito-Solana client as the low stake results in low probability of their bundles being included. Validators will not utilize the Jito-Solana client if there are few Searchers as the low MEV revenue is probably not worth the additional overhead.

Thesis

1. Solana’s MEV Market Size will continue to grow

As the Solana ecosystem continues to grow in liquidity and token variety, the market size for MEV is poised to expand significantly. The introduction of more assets and trading volume on DEXes creates a fertile ground for increased MEV opportunities. For instance, Jito recently passed an all time high from MEV revenue.

Activities like atomic arbitrage and liquidations become more prevalent and potentially more profitable. As the volume and frequency of trades rise, so does the potential for capturing MEV, thereby increasing the revenue generated from these activities.

2. Solana’s LST market share will increase

The relatively modest market share of liquid staking in Solana, approximately 4.5%, can be attributed to two key factors. Firstly, Solana has historically offered a brief unstaking period for its native stakers, diminishing the need for liquid staking alternatives. Secondly, the decline in DeFi activities has resulted in a reduced demand for SOL liquidity, further impacting the growth and adoption of liquid staking. With the proliferation of the next wave of DeFi protocols like Drift Protocol, MarginFi, Kamino, Meteora etc, utility and demand for LSTs will continue to grow. Most of the current LST supply is concentrated in lending/borrowing protocols and I expect that to expand to other categories in DeFi. As the only staking pool on the market that fully redistribute MEV revenue back to stakers, I expect JitoSOL to be the dominant utility LST that will be the second most used base asset other than SOL.

3. The Jito flywheel

The integrated MEV + LST design by Jito is unlike any other staking or MEV solutions out there in the market and truly encapsulates the “Jito = Lido + Flashbots” narrative. Combining both business models together creates an interesting flywheel that results in a formidable network effect that benefits the entire ecosystem. See diagram below for more details.

4. Value will eventually accrue to $JTO

Currently, there are two synergistic sources of revenue - the staking pool and the block engine. The revenue from the staking pool accrues back to the Jito DAO while the latter accrues to Jito Labs. I have to reemphasize that the block engine accrued revenue is not only from validators in the Jito stake pool but from ALL validators running the Jito-Solana client. The Jito-Solana current network stake is around 45% and I expect this to increase with more interest in MEV revenue and running the Jito-Solana client over the native Solana client only has incremental revenue. Governance will probably engage in discussions around allocating some of the block engine revenue back to the Jito DAO in the future.

There are also other possible ways for $JTO to accrue more value in the future. Block Engines are currently only operated by Jito Labs in Amsterdam, Frankfurt, NY and Tokyo. As more searchers enter the picture and want to be closer to block engines to gain an edge in latency, I expect future block engines to be operated by third parties which might represent an additional form of revenue source for the Jito DAO. The future implementation of StakeNet could also be an interesting angle here. How can we ensure that the keepers in the StakeNet network are doing their jobs efficiently? What if keepers are required to stake $JTO in order to gain access to a share of the stake pool revenue?

Conclusion

Jito is backed by a stellar team who led and built the foundations of a MEV infrastructure on Solana that not only benefits Jito but really the entire ecosystem. Ultimately, I believe Jito is best positioned to capture value from both the growing market size of Solana MEV and increased adoption of LSTs.